The International Debt Report 2025 (IDR 2025) arrives at a moment when sovereign debt has become one of the most binding constraints on development in low- and middle-income countries. The report does not describe a temporary disruption. Instead, it documents a structural shift in global finance. External debt, once viewed as a mechanism for accelerating development, has increasingly become a channel through which resources flow out of poorer economies. This shift is occurring alongside other pressures, including climate-related disasters, volatile food and energy prices, and tightening global financial conditions.

What distinguishes the current moment is not only the scale of debt, but its consequences. Countries that entered the pandemic with limited fiscal space now face repayment obligations that restrict investment in health, education, and infrastructure.

As World Bank Chief Economist Indermit Gill has argued, high debt repayments are no longer a background issue. They are “crowding out spending on development and poverty reduction,” and doing so at a time when needs are rising rather than falling. The IDR 2025 provides empirical grounding for this concern (Gill, as cited in The Guardian, 2024).

External debt in a period of sustained global stress

One of the most significant findings of the IDR 2025 is the scale of net financial outflows from developing countries. Between 2022 and 2024, low- and middle-income countries paid approximately USD 741 billion more in debt service than they received in new external financing (World Bank Debt Statistics Team, 2025). This represents the largest net outflow recorded in over fifty years. It marks a reversal of the traditional role of external finance in development.

This reversal is closely linked to global interest rate dynamics. Even as inflation has eased in some advanced economies, borrowing costs for developing countries remain high. Many countries are refinancing older loans at interest rates that are double their pre-pandemic levels. These higher costs matter because most low-income countries borrow in foreign currency and cannot easily hedge against exchange rate risk. When domestic currencies depreciate, the real burden of debt rises immediately.

The situation is particularly acute in East Africa. In Kenya, the depreciation of the shilling against the U.S. dollar sharply increased the cost of servicing external debt between 2022 and 2024. Fiscal adjustment followed. Public investment was constrained, and social spending came under pressure. Ethiopia and Tanzania experienced similar dynamics, though with less access to international capital markets. In these cases, limited refinancing options amplified the impact of global tightening (World Bank Debt Statistics Team, 2025).

Why high debt hurts poor countries more than rich ones

The IDR 2025 makes clear that debt vulnerability is not determined by debt levels alone. High-income countries often carry public debt exceeding 100 percent of GDP. Yet they remain solvent and attractive to investors. Their advantage lies in institutional credibility, deep domestic capital markets, and the ability to borrow in their own currencies.

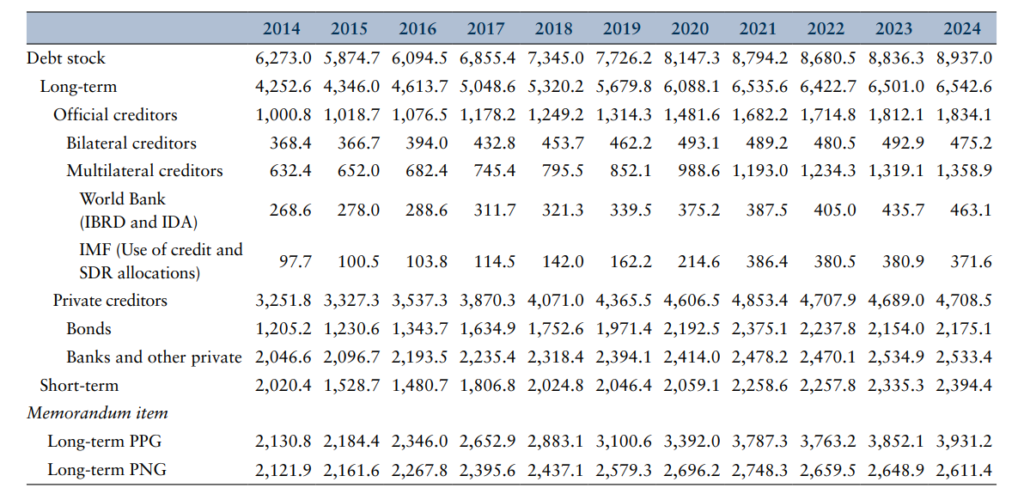

External Debt Stock of Low- and Middle-Income Countries, 2014–24 in US$ (billion)

Note: IBRD = International Bank for Reconstruction and Development; IDA = International Development Association;

IMF = International Monetary Fund; PNG = private nonguaranteed; PPG = public and publicly guaranteed; SDR = special

drawing right.

Low-income countries operate under very different conditions. Their debt is largely external, foreign-currency denominated, and shorter in maturity. This exposes them to sudden shifts in investor sentiment and exchange rate volatility. Even modest shocks can translate into fiscal crises.

East African countries illustrate this asymmetry well. Rwanda, often cited as a case of disciplined fiscal management, has nonetheless seen its debt service obligations rise steadily as externally financed infrastructure projects mature. By 2024, debt servicing absorbed a growing share of domestic revenue. This occurred despite debt-to-GDP ratios that remain moderate by global standards. The issue is not excessive borrowing alone. It is the cost and structure of that borrowing.

Kenya’s experience is more severe. In several recent fiscal years, external debt service has exceeded public spending on health. This reflects both the size of Kenya’s external obligations and the high interest rates attached to them. Such trade-offs are rarely faced by advanced economies. They are, however, increasingly common across Sub-Saharan Africa (World Bank Debt Statistics Team, 2025).

Shifting creditors and the return of net outflows

Another critical insight from the IDR 2025 concerns changes in creditor composition. Over the past decade, non-Paris Club lenders, particularly China, became major financiers of infrastructure across Africa. These loans supported roads, energy projects, and transport corridors. However, the lending cycle has now turned.

New lending from China has declined sharply. At the same time, repayments on existing loans have continued to rise. According to Reuters, many African countries now send more money to China in debt repayments than they receive in new loans (Reuters, 2026). This has transformed what was once a source of development finance into a channel of net resource outflow.

For countries such as Ethiopia and Kenya, this shift has tightened liquidity. Debt obligations remain fixed, while fresh inflows have slowed. Unlike advanced economies, these countries cannot simply roll over debt. Repayment is unavoidable, and fiscal space shrinks as a result.

What this means for poor countries: Expert perspectives

The empirical patterns documented in the International Debt Report 2025 closely mirror concerns that development economists have raised for more than a decade. What distinguishes the current moment is that these concerns are no longer theoretical. They are now visible in fiscal outcomes, social budgets, and growth trajectories across low-income countries. From different intellectual traditions, prominent economists converge on a shared diagnosis: the global debt system places disproportionate adjustment costs on poorer economies.

Joseph Stiglitz has long argued that sovereign debt crises in developing countries are not primarily the result of fiscal irresponsibility, but of structural asymmetries in global finance. In recent commentary on the post-pandemic debt environment, he warned that existing debt resolution mechanisms are “designed to protect creditors, not societies,” and that prolonged debt servicing locks countries into low-growth equilibria (Stiglitz, as cited in CAFOD, 2025). The IDR 2025 lends empirical weight to this claim. Rising interest payments documented in the report show how debt servicing absorbs resources that could otherwise finance education, health, or climate adaptation. In this sense, debt does not merely reflect economic weakness; it actively reproduces it.

Carmen Reinhart’s work on debt crises offers a complementary but distinct perspective. Reinhart has emphasized that debt distress often emerges well before formal default, through what she terms “debt intolerance.” This condition arises when countries with limited institutional capacity face borrowing costs that far exceed those of advanced economies at similar debt levels. The IDR 2025 illustrates this clearly. Countries such as Rwanda or Tanzania face growing fiscal strain at debt ratios that would be considered manageable in advanced economies. Reinhart’s framework helps explain why. Vulnerability is not about debt size alone, but about credibility, currency denomination, and exposure to sudden capital reversals. For poor countries, these vulnerabilities accumulate quickly.

Thomas Piketty approaches the issue from the perspective of global inequality. He has argued that international debt relations often replicate colonial-era patterns of extraction, where capital flows outward while adjustment costs remain domestic. In recent debates on sovereign debt and development, Piketty has stressed that when poor countries devote a growing share of national income to external creditors, inequality between nations deepens even if global GDP grows. The IDR 2025 supports this argument by documenting sustained net financial outflows from developing countries during a period of rising global wealth. For low-income countries, growth without fiscal space translates into limited improvements in living standards.

Dani Rodrik adds another layer to this analysis by linking debt to policy autonomy. Rodrik has repeatedly emphasized that development requires “policy space” -the ability of governments to experiment, invest, and respond to shocks. High debt service obligations, he argues, narrow this space dramatically. The IDR 2025 shows how this dynamic plays out in practice. When governments prioritize debt repayment to maintain market access, they often postpone public investment or adopt contractionary fiscal policies. Over time, this undermines growth and weakens the very capacity needed to service debt sustainably. From Rodrik’s perspective, debt becomes a constraint on state capability, not just on budgets.

Ricardo Hausmann, writing from the perspective of growth diagnostics, highlights another critical dimension. He argues that debt becomes particularly damaging when countries lack diversified export bases. Without sufficient foreign exchange earnings, debt service pressures intensify regardless of fiscal discipline. This insight is especially relevant for East African economies. Many rely on a narrow range of exports, making them vulnerable to price fluctuations and external shocks. The IDR 2025 shows that even when borrowing finances infrastructure, weak export performance can limit its capacity to generate the foreign exchange needed for repayment. In such contexts, debt amplifies external vulnerability rather than reducing it.

From within the policy community, World Bank Chief Economist Indermit Gill has offered one of the clearest institutional critiques. He has warned that the current debt environment risks reversing decades of development gains if repayment pressures continue to rise unchecked. In his assessment, high debt service costs are “crowding out development spending at exactly the wrong time,” particularly as countries face climate shocks and demographic pressures (Gill, as cited in The Guardian, 2024). The IDR 2025 provides concrete evidence for this concern. It shows that debt pressures are not evenly distributed, but are concentrated in countries with the least capacity to absorb them.

Taken together, these perspectives converge on a critical conclusion. For poor countries, debt is no longer simply a financing tool. It has become a structural constraint that shapes policy choices, limits social investment, and reinforces global inequality. The IDR 2025 does not contradict this body of thought; it confirms it with data. The challenge, therefore, is not only to manage debt more efficiently, but to rethink the rules and institutions that govern sovereign borrowing and repayment in an unequal world.

The future of international debt

The IDR 2025 does not suggest that debt pressures will ease quickly. Instead, it points toward a future marked by constrained choices. Multilateral institutions have increased their lending, but their resources are insufficient to replace declining bilateral and private flows. As a result, many countries are turning to domestic debt markets.

Kenya and Rwanda have both expanded domestic bond issuance in recent years. This has reduced foreign exchange risk. However, it has also increased domestic interest rates. Private sector credit has become more expensive. Growth has slowed. These trade-offs highlight that domestic borrowing is not a cost-free solution.

The report also emphasizes debt transparency. Improved reporting has revealed liabilities that were previously hidden, particularly those linked to state-owned enterprises and public-private partnerships. While this transparency can initially raise concerns, it is essential for credible fiscal management and informed policy decisions.

Coping with debt repayment pressures

The evidence points toward several lessons. First, domestic revenue mobilization is critical. Countries with stronger tax systems are better able to service debt without cutting essential spending. Rwanda’s gradual improvements in tax administration demonstrate how incremental reforms can strengthen fiscal resilience.

Second, the quality of borrowing matters. Debt used to finance productive investment, particularly in export-oriented sectors, offers a clearer path to sustainability. Debt used to cover recurrent expenditure does not.

The international reform is necessary. Existing debt restructuring mechanisms remain slow and fragmented. Indermit Gill has warned that without faster and more coordinated processes, countries will remain trapped in repeated cycles of crisis and adjustment (Gill, as cited in The Guardian, 2024). Innovative tools, such as debt-for-climate swaps, offer promise. However, they cannot substitute for deeper reform of the global debt architecture.

In a nutshell, The International Debt Report 2025 presents a clear and unsettling message. The global debt system is increasingly imposing its heaviest costs on those least able to bear them. For low-income countries, particularly in East Africa, debt servicing now competes directly with development priorities. The report shows that this is not the result of isolated policy failures. It reflects structural features of the international financial system.

Without meaningful reform, debt will continue to function as a constraint rather than a catalyst for development. The challenge ahead is not only technical. It is political. It requires rethinking how risk, responsibility, and adjustment are shared in a deeply unequal global economy.

{kind=link}